In Brief: What Is the “K-Shaped” Economy?

The eleventh letter of the alphabet has taken on new meaning. The letter “K” is now used to describe the bifurcation in today’s economy. Different consumer segments and the businesses that serve them are growing at different rates. Indeed, there’s a divergence: The upward-slanting arm of the “K” represents higher-income households with strong consumer spending, fuelled by healthy income growth and rising wealth. In contrast, the downward-slanting arm represents low- and middle-income households facing rising living costs, stagnant wages and higher debt burdens.

Since consumer spending drives more than two-thirds of total U.S. GDP, this divide carries implications. Higher-income households are now responsible for a disproportionate share of economic activity. In Q2 2025, the top 10 percent of income earners accounted for nearly half of all U.S. consumer spending. This imbalance underscores how economic resilience has become concentrated among wealthier consumers—those benefiting most from asset price appreciation. As a result, the softer labour-market figures observed in 2025 that largely impacted lower-income households attracted less attention as they didn’t materially affect overall consumption.

Where are economies and markets headed in 2026? In 2025, artificial intelligence (AI) was a key driver of market enthusiasm. If AI capital investments deliver productivity gains, markets may look past ongoing labour-market weakness, effectively shrugging off the lower part of the K—although expectations may already be partly reflected in valuations. At the same time, monetary stimulus from interest rate cuts in Canada and the U.S., tariff renegotiations and potential U.S. tax refunds could strengthen labour markets and support more exposed sectors. Yet some argue the same stimulus has exacerbated wealth inequality.

Where are economies and markets headed in 2026? In 2025, artificial intelligence (AI) was a key driver of market enthusiasm. If AI capital investments deliver productivity gains, markets may look past ongoing labour-market weakness, effectively shrugging off the lower part of the K—although expectations may already be partly reflected in valuations. At the same time, monetary stimulus from interest rate cuts in Canada and the U.S., tariff renegotiations and potential U.S. tax refunds could strengthen labour markets and support more exposed sectors. Yet some argue the same stimulus has exacerbated wealth inequality.

As advisors, we continue to navigate the evolving landscape. The “K-shaped” economy reinforces the value of time-tested principles—diversification, a focus on quality and ongoing risk management—as key to successful long-term wealth management in an increasingly uneven economic environment.

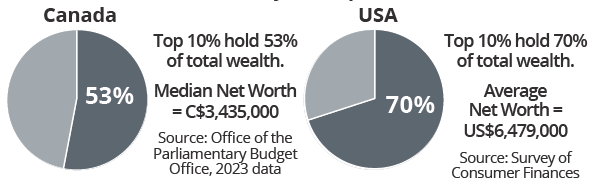

Share of Total Wealth Held By the Top 10% (2023 Data)