Is the Small-Cap Surge Here to Stay?

Since October 2025, U.S. small-cap stocks have staged a notable comeback, outperforming large-cap growth stocks as investors look beyond years of dominance by tech mega-caps. This has prompted the question: Is this a temporary bounce, or the start of a more meaningful trend?

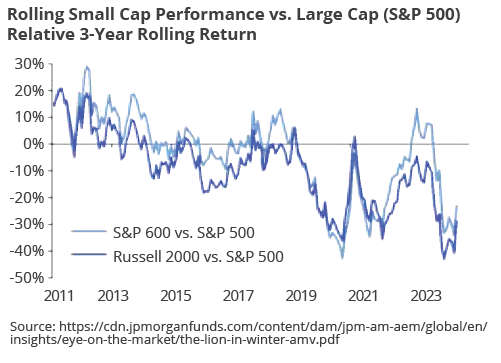

Small Caps vs. Large Caps

In the U.S., small-cap stocks are generally defined as companies with a market capitalization (share price multiplied by shares outstanding) between $250 million and $2 billion. The Russell 2000 and S&P 600 are the most commonly used U.S. small-cap benchmarks. In Canada, where markets are smaller, small caps are generally considered to have a market capitalization of $1.5 billion or less. In contrast, a large-cap stock generally refers to a company with a market capitalization exceeding $10 billion.

In the past, small caps were seen as attractive opportunities for those investors willing to take on more risk in exchange for potentially higher returns. These firms were perceived to have higher growth potential, as well as strong merger and acquisition prospects.

Yet, since 2010, small caps have largely underperformed large cap stocks (see graph for relative performance) and have traded at some of their lowest levels in decades. The current cycle happened for a reason. Large caps have had stronger earnings and better free cash flow margins, while small caps exhibit much lower profitability. Small caps often carry higher debt positions (relative to earnings) and are more exposed to interest rate changes due to floating rate debt and shorter average maturities. Rising interest rates between 2022 and 2024 placed significant pressure on many small caps with rate-sensitive debt. In addition, small caps tend to be more sensitive to economic cycles than their large-cap counterparts.

At the same time, many higher-quality small-cap companies are not listing publicly, instead being taken private by private equity firms before reaching scale. Private markets have grown dramatically: In 2000, private equity and venture capital firms managed around $600 billion in assets; today, assets under management exceed $10 trillion. This shift has resulted in a greater proportion of lower-quality companies entering small-cap indices, which has challenged overall returns.

Why the Rotation Into Small Caps Over Recent Months?

As valuations for tech mega-cap growth stocks remained well above historical averages, investors turned to more undervalued sectors. Recent easing of cyclical headwinds, particularly higher interest rates that previously pressured small-cap valuations, has created a more favourable environment for these companies. A weaker U.S. dollar has further benefited small-cap firms with foreign revenue exposure, while improvements in the U.S. regional banking sector have helped support broader small-cap business activity. Ongoing fiscal stimulus measures provide an additional layer of support, enhancing the potential for selective opportunities within the sector.

A Selective Approach

The small-cap universe is highly diverse, with significant variation in company quality and performance. As with many aspects of successful investing, a selective approach can help investors manage structural risks while identifying businesses with stronger balance sheets, earnings resilience and longer-term potential. Even with a more favourable environment emerging for the sector, ongoing economic uncertainty makes disciplined, quality-focused stock selection increasingly important.