The FHSA: Six Savvy Tips for Investors

Spring’s arrival brings home-buying season, making it an opportune time to revisit a valuable tool that supports the purchase of a first home: the First Home Savings Account (FHSA). The account offers tax-deductible contributions, tax-free growth and tax-free withdrawals for qualifying home purchases. Generally, you must be a “first-time homebuyer” who is a Canadian resident over the age of majority, but not older than 71 on December 31 of the year in which the account is opened.

Here are six tips to make the most of the FHSA:

1. Even if you’ve owned a home before, you may still qualify. If you or your spouse/partner has owned a house in the past, you may still qualify if you haven’t owned a home in the current year and in the preceding four calendar years. People also often assume that FHSAs are just for young buyers. However, “seasoned” investors who haven’t owned a home in recent years might consider opening one, even if it isn’t used for a home purchase, as it may act as a retirement savings boost (see point #6, below).

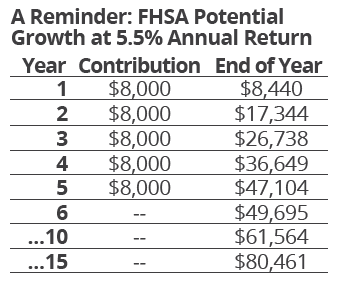

2. Maximize contributions early for compounded growth. The FHSA allows annual contributions of up to $8,000, with a lifetime limit of $40,000. However, the FHSA must be closed by December 31 of the earliest of: the 15th anniversary of opening, the year following the first qualifying withdrawal or the year the account holder turns 71. As such, not contributing the full $8,000 each year risks missing out on the lifetime limit, its tax deductible benefits and the potential for tax-free growth  over time. Consider the scenario in which an investor contributes the maximum each year from the outset. At a 5.5 percent annual return, by year 5, the $40,000 contribution could grow to $47,104. By year 15, it could grow to over $80,000; all tax free upon withdrawal for the purchase of a first home.

over time. Consider the scenario in which an investor contributes the maximum each year from the outset. At a 5.5 percent annual return, by year 5, the $40,000 contribution could grow to $47,104. By year 15, it could grow to over $80,000; all tax free upon withdrawal for the purchase of a first home.

3. Carry forward contributions for future tax savings. Like a Registered Retirement Savings Plan (RRSP), FHSA contributions are tax-deductible, and any unused deductions can be carried forward to a future year, even beyond the closure of your FHSA.1 If you expect to be in a higher tax bracket in a future year, claiming the deduction later may help maximize your tax savings.

4. Be aware that the “carry-forward” rules differ from other registered plans. This has been a source of some confusion. For the FHSA, an account holder can contribute $8,000 in annual participation room. Unused amounts can be carried forward to the following year, but only to a maximum of $8,000 and subject to a lifetime limit of $40,000. This differs from the Tax-Free Savings Account (TFSA) and RRSP, where unused contribution room is carried forward indefinitely (to age 71 for the RRSP); there is no limit. Take, for example, an individual who opened the FHSA in 2024 and contributed $4,000. In 2025, the FHSA would have $12,000 in participation room: $8,000 of new room for 2025 and $4,000 carried forward from 2024. If they do not contribute in 2025, they would have $16,000 of participation room in 2026, not $20,000, as only $8,000 carries forward from 2025. Excess contributions are subject to a penalty of one percent per month. 5. Combine the FHSA with the RRSP Home Buyers’ Plan (HBP). You can use the FHSA alongside the RRSP’s HBP. As of 2026, the HBP now allows you to withdraw up to $60,000 from your RRSP for a first-home purchase without tax consequences, subject to HBP repayment rules. Using the scenario above, if the FHSA grows to $80,000 and you use the full RRSP HBP, you could have $140,000 toward your first home.

5. Combine the FHSA with the RRSP Home Buyers’ Plan (HBP). You can use the FHSA alongside the RRSP’s HBP. As of 2026, the HBP now allows you to withdraw up to $60,000 from your RRSP for a first-home purchase without tax consequences, subject to HBP repayment rules. Using the scenario above, if the FHSA grows to $80,000 and you use the full RRSP HBP, you could have $140,000 toward your first home.

6. Transfer unused FHSA funds to an RRSP or RRIF. If you do not use the FHSA to purchase a first home, assets can be transferred tax-free to an RRSP or Registered Retirement Income Fund (RRIF), essentially giving you additional contribution room for retirement savings.

1. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account/tax-deductions-fhsa-contributions.html